HMRC have released new data on the High Income Child Benefit Charge

The High Income Child Benefit Charge (HICBC), introduced in January 2013, remains a prime example of how not to design and operate a tax. As a reminder, the aim of HICBC is to make any Child Benefit recipient repay some or all of their Child Benefit back (as tax) if they or their partner has an individual adjusted net income exceeding £50,000 per year. The repayment is at the rate of 1% of total benefit paid for each £100 of income above the threshold, up to £60,000, at which point the tax charge matches the total benefit. Among the HICBC’s many flaws are:

- The £50,000 threshold has been unchanged since its introduction. At the time the higher rate tax threshold was £42,475, so arguably there was initially an element of ‘high income’ to the HICBC. Now, a basic rate taxpayer is just within its ambit. Had indexation applied, the HICBC threshold would now be around £65,000.

- The effective rate of the HICBC tax rises as child benefit rates increase. For example, for a family with two children the effective tax rate was 18.85% in 2022/23 and is now 20.75% in 2023/24.

- A couple with joint income of £100,000 split equally would suffer no HICBC, while one in which there was a sole earner with income of £60,000 would pay the maximum HICBC.

- There is no consistency with other elements of child tax and benefit policy. For example, the free childcare provisions, which were given a boost in March’s Budget, have a cliff edge income threshold of £100,000 per individual. Stranger still, there are situations where Universal Credit is payable even when all Child Benefit entitlement has been removed by the HICBC.

The latest statistics from HMRC on Child Benefit highlight the distortions that HICBC has created:

- 7.70 million families claiming Child Benefit, but only 7.01 million families are in receipt of Child Benefit payments. The missing 690,000 are families where benefit is claimed to secure entitlement NIC credits, but no Child Benefit is paid because HICBC would nullify it. Lack of awareness of the need to claim Child Benefit, thereby triggering automatic NIC credits, is another system flaw.

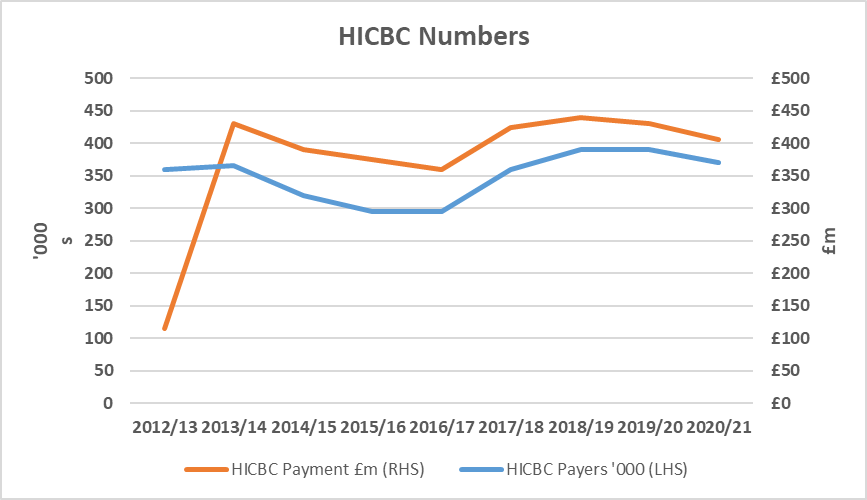

- In 2020/21, the latest year for which figures are available, 355,000 people paid £405m in HICBC, figures which HMRC estimate need a 4% uplift ‘in response to late tax returns or compliance activity’. If we adjust for this, the pattern of HICBC payers and their payments looks like this:

- The HMRC data used in the above graph is only part of the story. In practice it probably mostly shows only those whose income sits between £50,000 and £60,000, where there is no logical option other than to take the Child Benefit payment and then hand some of it back as HICBC. The HMRC data is silent on the number for whom NIC credits are irrelevant, such as some two earner couples, and who thus choose to make no Child Benefit claim.

Comment

The HICBC can increase the effective rate of tax relief pension contributions as these reduce adjusted net income.

This is an example of one of the recent news bulletins that was posted on our Techlink website. Signing up to Techlink will give you access to original articles, like this, on a daily basis. Techlink also provides you with a comprehensive (and searchable) library of information, daily bulletins on developments of relevance to the industry, multimedia learning and professional development tools. Techlink can also be your ‘gateway’ for accessing consultancy through our ‘ASK’ service which enables you to receive responses to your technical questions from our highly trained technical consultants.

You can sign up for a free 30 day trial of Techlink at anytime. For more information go to www.techlink.co.uk