The day was marked by 23 announcements, but few were of great interest

Tax Administration and Maintenance Day (TAMD) is an opportunity for the Treasury to publish a range of documents (consultation, responses, calls for evidence, etc.) that would otherwise add to the paper mountain created on Budget Day. This year’s TAMD contained a few interesting nuggets amongst plenty of meh material. First, the more interesting stuff:

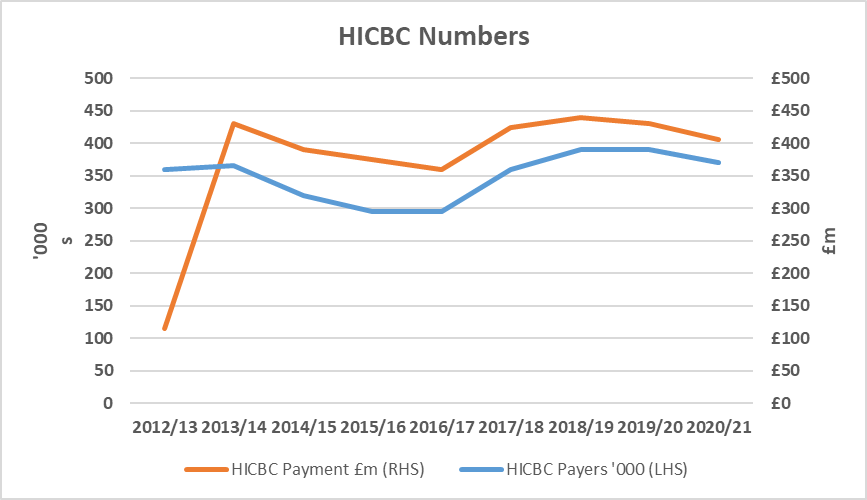

National Insurance (NIC) credits We commented in a recent Bulletin on the messy combination of the High Income Child Benefit Charge, claims for Child Benefit and NIC credits. Now the Government says it will act on this issue so that affected parents who failed to claim NIC credits will receive them retrospectively. Further details will emerge ‘in due course’.

Stamp Taxes on Shares The Government has published a consultation on proposals to modernise and rationalise the framework for Stamp Taxes on Shares. The consultation raises the possibility of replacing the current dual framework of Stamp Duty and Stamp Duty Reserve Tax with one securities tax.

Off-payroll working The Government has published a consultation on a possible legislative change to address the over-collection of tax that can arise when the off-payroll working rules (also known as IR35) are not properly complied with. In such circumstances, the deemed employer is liable for the full PAYE liability due on the worker’s income, but the worker and their personal service company may have already paid tax and NICs on the same income. This consultation suggests a potential change to allow HMRC to set off the worker’s tax and NICs already paid against the employer’s PAYE liability.

Umbrella companies Some things do not arrive on time…so a summary of responses will be published shortly to a call for evidence on the umbrella company market launched in 2021. At the same time, a fresh consultation will be issued reviewing policy options for the umbrella company market.

Information and data A call for evidence on information and data powers has been published as part of the Tax Administration Framework Review (TAFR). The focus is on standardising data provision from third parties, creating more flexible legislation (!), pre-population of tax returns and trying to bring more consistency between different tax regimes.

HMRC sandbox The Government has published a discussion document on a potential new legislative approach that HMRC could use for piloting tax changes (a ‘sandbox’, borrowing FCA jargon).

Employee Ownership Trusts (EOTs) Later in 2023 there will be a consultation on the ‘use and effectiveness’ of the EOT tax regime. HMRC wants to be sure that the reliefs available are not being used for tax planning purposes that it had not envisaged.

Now the less interesting material:

Repayment agents In January, the Government announced that income tax repayment agents would be required to register with HMRC. The deadline for registration has now been set as 2 August 2023, along with details of how to register with HMRC and the exemptions available (including for those who do not charge any fee for submitting repayment claims).

Help to Save The Help to Save scheme was extended to April 2025 in the March Budget. The Treasury has now issued a consultation on the scheme’s design aiming for simplification and greater take up by those with low income.

Reserved Investor Fund A consultation has been published by HMRC and the Treasury on (yet another) new type of investment fund: the Reserved Investor Fund (RIF). RIFs would be directed at professional and institutional investors, with the broader retail investment market excluded.

Taxation of Decentralised Finance lending and staking The demise of FTX has not stopped the Government publishing a response to the call for evidence on the taxation of crypto-asset transactions in Decentralised Finance (DeFi) lending and staking. Simultaneously, a consultation has been published potential amendment to the tax rules so that they ‘better reflect the substance of these arrangements’.

Construction Industry Scheme (CIS) A new consultation proposes reforms to the CIS, including strengthening the tests for Gross Payment Status (GPS) and some administrative simplifications, such as excluding from the CIS most payments made by commercial landlords to tenants.

Diverted profits tax, transfer pricing and permanent establishment reform Next month a consultation will be published on simplifying and updating legislation for:

- diverted profits tax (increased rate on diverted UK profits);

- transfer pricing (related party transactions); and

- permanent establishments (right to tax non-resident entities with a UK business presence).

Charities compliance A consultation on tax compliance for charities has been published indicating that HMRC thinks ‘some rules are not working as intended.’ The consultation covers areas such as:

- preventing donors from obtaining a financial benefit from their donation;

- preventing abuse of the charitable investment rules;

- closing a gap in non-charitable expenditure rules; and

- sanctioning charities that do not meet their Filing and Payment Obligations.

Data gaps Following publication of a summary of responses to HMRC’s consultation on improving the data it collects. the Government will start – after the necessary legislation passes – collecting new data on self-employed start/end dates, employee hours worked, and dividends paid in owner-managed businesses. It will be interesting to see what it does with the data.

Tackling promoters of tax avoidance. The Government has published a consultation on the introduction of a new criminal offence for promoters of tax avoidance who fail to comply with a legal notice from HMRC to stop promoting a tax avoidance scheme. It is also consulting on speeding up disqualification of directors of companies involved in promoting tax avoidance.

This is an example of one of the recent news bulletins that was posted on our Techlink website. Signing up to Techlink will give you access to original articles, like this, on a daily basis. Techlink also provides you with a comprehensive (and searchable) library of information, daily bulletins on developments of relevance to the industry, multimedia learning and professional development tools. Techlink can also be your ‘gateway’ for accessing consultancy through our ‘ASK’ service which enables you to receive responses to your technical questions from our highly trained technical consultants.

You can sign up for a free 30 day trial of Techlink at anytime. For more information go to www.techlink.co.uk