Employer’s National Insurance Contributions (NICs), which it is looking increasingly likely will be increased in the Budget. It looks an easy revenue-raiser, but is it?

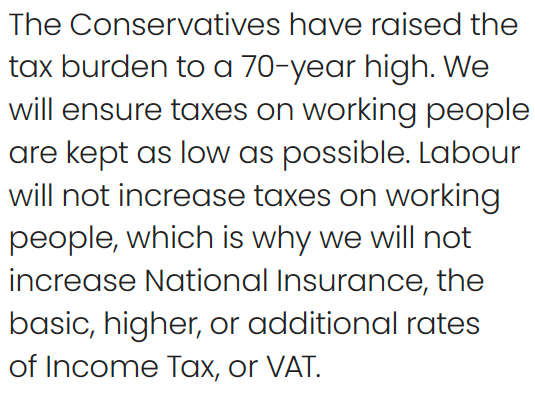

Here is the paragraph on page 21 of the Labour manifesto which is currently causing what might be described as a certain amount of controversy:

It is the only mention of the words ‘National Insurance’ in the entire manifesto. Labour’s stance is that the reference to ‘working people’ means that it is clear the pledge is not referring to employer’s NICs.

While the Conservatives are now disputing that claimed clarity, during the election campaign the then Chief Secretary to the Treasury, Laura Trott (now the Shadow), flagged up the possibility of employer’s NIC rises in a document entitled ‘Labour’s 18 Tax Rises’. In response, Labour’s shadow ministers refused to make a commitment to keep employer’s NICs rates unchanged.

Leaving aside the political gaming, what would be the effect of a rise in employer’s NICs?

- HMRC’s ready reckoner says an extra one percentage point on the employer’s Class 1 rate in 2024/25 (taking it to a main rate of 14.8%) would raise £8.45bn in 2025/26 and £8.9bn in 2027/28.

- The impact of applying employer’s NICs to employer pension contributions is not covered by the ready reckoner. HMRC data puts the total employer NIC savings/relief on employer’s contributions at £15.4bn in 2022/23. This suggests that each one percentage point of NIC on pension contributions would yield £1.1bn-1.2bn.

- There is a major qualification to both these estimates: the biggest single UK employer is the government. Thus, an increase in employer’s NICs would lead to higher departmental expenditure requirements or, if it was not compensated for, spending cuts. On the pension front the impact is very significant: £5.3bn of the employer’s NICs relief related to public sector pension schemes.

- Just to muddy the water a little more, the HMRC data shows that £2.6bn (17%) of all employer’s relief related to salary sacrifice contributions. £2.3bn related to the private sector.

- From an economic viewpoint, raising employer’s NICs is generally considered to ultimately impact on employees, making the ‘not increase taxes on working people’ an awkward statement for the Government to justify.

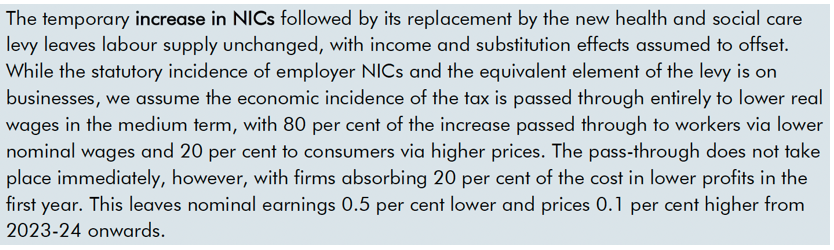

- For proof, look no further than the Office for Budget Responsibility (OBR)’s Economic and Fiscal Outlook for October 2021 and its comments on Rishi’s Sunak’s introduction of a brief 1.25% NICs rise followed by the short-lived Health and Social Security Levy:

The OBR’s views were reinforced at the time by the then Shadow Chancellor, Rachel Reeves:

- A further economic criticism is that if only employer’s NICs were increased, this would add to the distortions in the tax system between salary, dividends and self-employed earnings. These have been shrinking as a consequence of the employee and self employed NICs reductions.

Comment

We have said before that the great political advantage of NICs is that the Great British public does not understand them. This has been well demonstrated by the cuts to employee’s NICs, which were equivalent to 4p off the basic rate of tax but produced no obvious political advantage for the last Government.

This is an example of one of the recent news bulletins that was posted on our Techlink website. Signing up to Techlink will give you access to original articles, like this, on a daily basis. Techlink also provides you with a comprehensive (and searchable) library of information, daily bulletins on developments of relevance to the industry, multimedia learning and professional development tools. Techlink can also be your ‘gateway’ for accessing consultancy through our ‘ASK’ service which enables you to receive responses to your technical questions from our highly trained technical consultants.

You can sign up for a free 30 day trial of Techlink at anytime. For more information go to www.techlink.co.uk.