In the run up to last month’s Autumn Budget, there was the usual will-he-won’t-he debate about whether the Chancellor would apply the triple lock to the State Pension. In the event there was none of the tweaking that occurred for the 2022 increase, so earnings growth (8.5%) was applied rather than CPI inflation (6.7%) or the floor (2.5%). As the graph above shows, the triple lock has danced around between all three options since it began life in 2011. The net effect is that in 2024/25 the State Pension will be 73.6% above its 2010/11 level, compared with cumulative earnings increases over the same period of 52.2% and price increases of 51.9%. Although that period is unusual in the virtual disappearance of real wage growth, the numbers highlight the affordability question that looms over the triple lock.

The Institute for Fiscal Studies (IFS) has looked at this topic many times and has now returned to it as part of a major Pension Review, undertaken in partnership with the abrdn Financial Fairness Trust. A new IFS report, ‘The future of the state pension’, sets out the challenges facing the State Pension and proposes a four-point guarantee as the new way forward.

The challenges

- The ageing population will add considerable pressure on public finances in coming decades. According to the projections from the Office for Budget Responsibility (OBR), spending on the State Pension and other pensioner benefits will rise from 5.9% of GDP (£152bn) in 2023/24 to 7.6% of GDP (£197 billion in today’s terms) by 2050/51. The key drivers of this are a projected 25% more pensioners in 2050 and the triple lock.

- The triple lock ratchets up the value of, and spending on, the State Pension over time in a way that creates uncertainty around what the level of the State Pension will be relative to average earnings, and for the public finances. Compared with increasing the State Pension in line with average earnings, the IFS projects that the triple lock alone could cost anywhere between an additional £5bn and £40bn per year in 2050 in today’s terms. If that seems a wide range, look back at that graph.

- If the Government wants to rein in State Pension spending, then relying only on raising the State Pension Age to achieve this, rather than moving to less generous indexation, would hit those with lower life expectancy harder. The same increase in the State Pension Age has a larger proportional impact on the expected State Pension wealth of people who die at younger ages than for people who live longer. Similarly, people who die at younger ages do not benefit as much from the triple lock, which ratchets up the value of the State Pension over time. Groups with lower life expectancy include poorer people (compared with richer people).

- Despite its relative simplicity, there is a mixture of confusion and pessimism about the State Pension. Although the State Pension has increased at least as fast as inflation every year since 1975, polling conducted as part of the Pension Review revealed considerable scepticism about the future. 38% of respondents thought that State Pension rises will not keep up with inflation in the next ten years. Such pessimism extends to the survival of the State Pension: a third of respondents did not think the State Pension would exist in 30 years’ time.

The four-point guarantee

- A target level for the New State Pension will be set by the Government, expressed as a share of median full-time earnings to be achieved by a specified date. This echoes the approach to the National Living Wage (NLW), which in 2024 will reach its target of two thirds of median earnings (please see our earlier Bulletin). At present the State Pension is about 30% of median full-time earnings, which the triple lock will gradually – and randomly – ratchet up, if left in place.

The IFS considers it wiser for the Government to set a target and stick with it – as has happened with the NLW – rather than leave matters to the roll of the triple lock dice. Currently, each 1% increase as a proportion of median earnings would add about £5bn to the annual pensions bill. Increases in the State Pension would in the long run keep pace with growth in average earnings, which ensures that pensioners benefit when living standards rise.

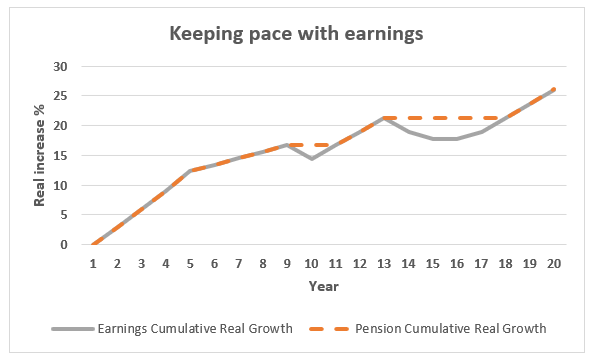

- The State Pension will continue to increase at least in line with inflation every year, both before and after the target level is reached. To the extent this inflation minimum increase is triggered, future increases would be constrained to achieve the long-term earnings-related growth goal. The effect is demonstrated in the graph below:

- The State Pension will not be means-tested.

- The State Pension Age will only rise as longevity at older ages increases, and never by the full amount of that longevity increase. To increase confidence and understanding, the Government will write to people around their 50th birthday stating what their State Pension age is expected to be. Their State Pension Age would then be fully guaranteed ten years before they reach it.

Comment

In recent years, the triple lock has increasingly looked to be on borrowed time. Its short-term survival will depend on next year’s election manifestos. If either of the two main parties says it will maintain the triple lock for the next Parliament, the other party may feel no alternative but to replicate the promise.

This is an example of one of the recent news bulletins that was posted on our Techlink website. Signing up to Techlink will give you access to original articles, like this, on a daily basis. Techlink also provides you with a comprehensive (and searchable) library of information, daily bulletins on developments of relevance to the industry, multimedia learning and professional development tools. Techlink can also be your ‘gateway’ for accessing consultancy through our ‘ASK’ service which enables you to receive responses to your technical questions from our highly trained technical consultants.

You can sign up for a free 30 day trial of Techlink at anytime. For more information go to www.techlink.co.uk.